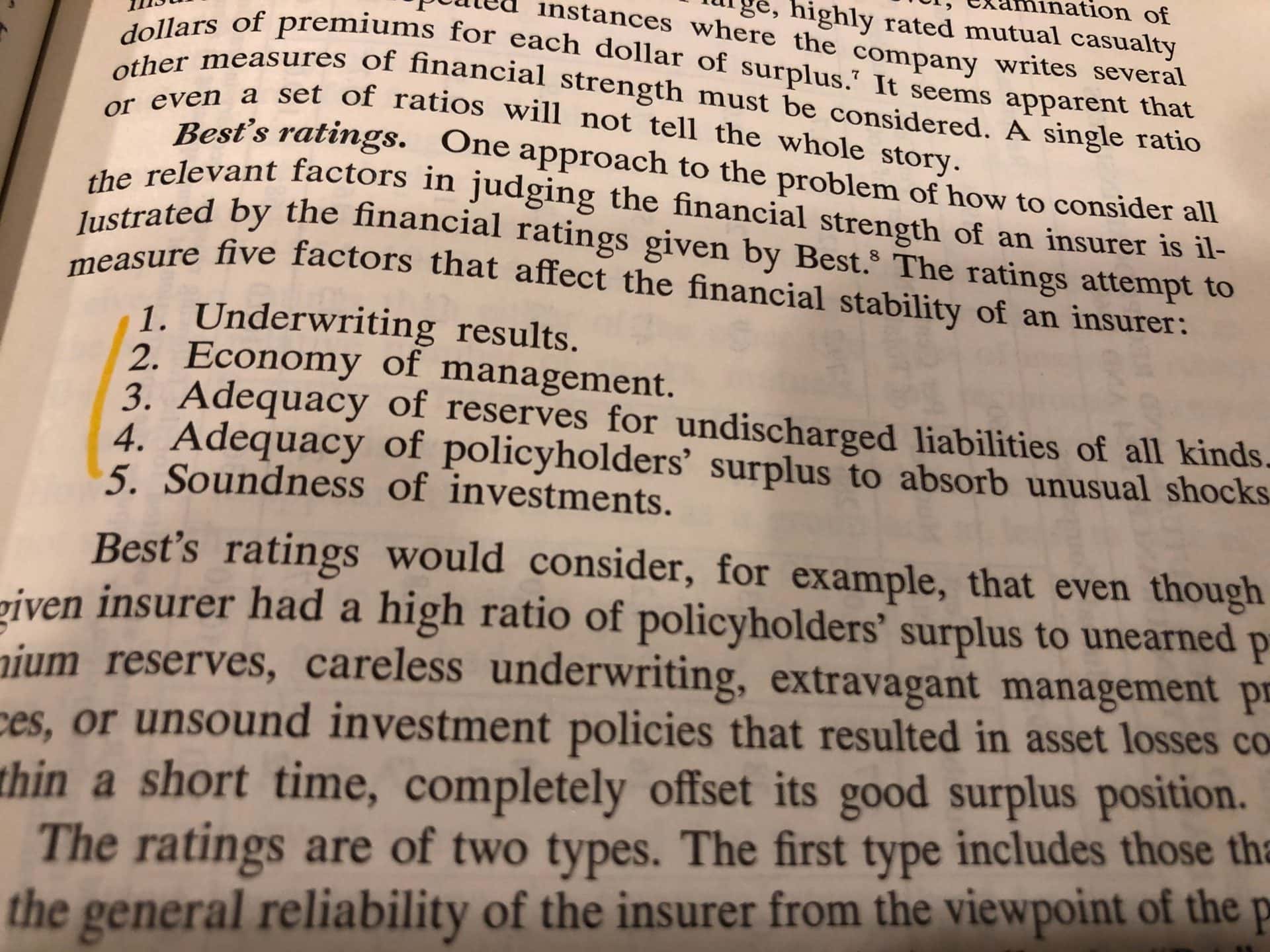

In the last blog, I wrote about the importance and the stability of insurance company operations. This is so important to the consumer because if the insurance company is not profitable and financially strong, they might have problems paying claims (and you don’t want that problem to be on your claim). If you did not check it out, take a look. So, I pick back up where I left off.

From an actuary to a sales department…

The Marketing Department takes the premium charges set by the insurance company’s actuaries and appoints trusted agents to build its business. The key word being “trust.” A trusted agent is necessary for the financial health of an insurance company. If the wrong policies are sold to the wrong policyholders at the wrong prices, in time the insurance company will be out of business or re-structured.

From premium collection to the investment department…

The insurance industry makes profit in several ways. One way is that they sell policies hopefully to enough people or businesses with low losses. Then, they take that cash flow from premiums and the profits from the results and invest them. Investment Departments of most insurance companies have very good results.

An appetite to grow…

Another affect on premium charge is an insurance company’s desire to grow its business in a certain market sector. When the insurance companies see that a certain area of industry is growing and seems to be profitable, they target that segment offering special insurance coverage at a special price.

Other than the policyholder working with the agent, there are at least three other “departments” working with policyholders…

The first is the Loss Control Department

Probably the most important service to policyholders are the services offered through the Loss Control Department. This department dispatches Safety Experts to conduct safety meetings, establishes loss control programs, inspect jobsites and equipment to reduce losses, etc. These experts then analyze with management the prior losses to prevent repeated occurrences. These are unheralded heroes who have helped businesses with their safety program, kept workers from being injured, and helped insurance companies avoid billions in losses through the years.

The second contact is the most feared department—the Audit Department

The premium audit task is performed by the Audit Department. “Audit” strikes fear and concern with most people because of negativity connected with outsiders putting their nose into financial records as a “sneaky way to get more money.” Perhaps, the insurance industry should rephrase the department “The Reconciliation Department” because reconciliation is what is really done anyway. With many commercial policies, policy premium determination is made between the final premium and the deposit premium after the policy term has expired.

The third contact is after a loss…

The Claim Department is where “the buck stops” for the insurance company and begins for the policyholder. This department exists and is the reason insurance is purchased. These knowledgeable insurance experts interpret the policy relating to a claim or circumstance and determine how much a claimant should receive, if any.

If you’d like to review your business or personal insurance, please call us at 423-763-1111. We hope to answer your questions and serve you!